Inside the Mind of Jamie Dimon

2 CEO types: Creator vs Preserver

There are two kinds of celebrity CEOs. The ones who create something from nothing, against the odds (think Musk), and the ones who preserve something and make it grow, also against the odds. The latter kind of CEO falls in and out of favor; Jack Welch used to be a role model, but GE’s performance since he pulled the ripcord has been lackluster. Jamie Dimon is another of the preserver-CEOs. - Byrne Hobart

“I’m not an artist, I’m not a tennis player, I’m not a musician, I’m not a politician. This is my contribution.”

Jamie Dimon is the third longest serving CEO of a major bank in the world. Twenty years at the helm of JP Morgan and its predecessor Bank One, he has managed his bank through two recessions and is in the midst of navigating a third.

Over that time he has seen his share price rise at an annual rate of 11%. People who once worked for him have fanned out and now run organisations all over the world including Standard Chartered, Wells Fargo, Barclays and First Data as well as operating at the highest levels of others including Comcast and Cerberus. A survey of investors ranks him among the top three CEOs in global financial services just behind Warren Buffett.

All of which suggests he has got something to teach. Fortunately, he provides it. Since 2000 he has written an annual letter to shareholders (which Warren Buffett calls one of the best). He also regularly appears on earnings calls, at investor conferences and as an interview guest. In my time as a hedge fund manager, I met him several times over the years myself. He presents with a consistency and clarity of thought that reveals some core ideas about business and life.

Here they are:

Fortress balance sheet

Jamie Dimon has always been ready for a crisis. While never forecasting the specifics of the crisis at hand, he has consistently cautioned that they are a feature of the landscape in which he operates. As long ago as 2002 he wrote in his shareholder letter “It’s hard to predict when a storm will happen, but one thing is inevitable: it will happen. We cannot control these events; we can barely predict them. Risk is not symmetrical. You can make a lot of money in the good times, but if you aren’t careful, you’ll go bankrupt in the bad.”

At one level it’s a simple observation. But it’s an observation company executives frequently ignore. Last week, car rental company Hertz filed for bankruptcy protection. Although the immediate cause was the collapse in bookings because of coronavirus travel restrictions, the seeds had been laid in a balance sheet bloated with too much debt and expensive legacy M&A.

Throughout his career, Jamie Dimon has preached the benefits of a ‘fortress balance sheet’ as a shield against the bad times. He introduced the concept to Bank One and carried it through to JPMorgan after the merger in 2004, sticking with it even while peers were sacrificing balance sheet strength for short-term earnings. In his 2007 shareholder letter he refers to a fortress balance sheet as a strategic imperative rather than simply a philosophical bent.

While his commitment to the idea of a strong balance sheet never changed, the underlying motivation behind it did. As a dealmaker with Sandy Weill before taking the Bank One job in 2000, the fortress balance sheet gave the wherewithal to make acquisitions during downturns, when assets were cheap. At Bank One, the fortress balance sheet was about ‘creating flexibility’. In his first letter to shareholders at JPMorgan in 2005, it was about the ability to ‘withstand – perhaps even benefit from – difficult times’. More recently, it has exclusively been about withstanding the difficult times. In 2014, Dimon couched his principle in broader, societal terms: “We have a huge obligation to society – not only must we never fail, but we need to be steadfast.”

Over the years, ‘fortress balance sheet’ has become less about creating value and more about preserving it. Perhaps, this is due to increased scale or a different environment, but it now seems to reflect a moral position rather than simply a financial one.

Obsession with the truth

Jamie Dimon has an absolute obsession with the truth. When asked at an event in Stanford in 2017 what leadership characteristics he looks for he said, “Character is a sine qua non. And by character, I also mean that they tell the truth, the whole truth and nothing but the truth. They don’t shave the truth, and they say the same thing to you that they do to you.” Dimon credits the notion of ‘shaving the truth’ to former Merrill Lynch CEO Daniel Tully who advised him never to tolerate it in 1996. The principle of saying the same thing to everyone permeates his every communication be it with the market, his employees, his customers or his board. “I always felt as a matter of principle inside a company if I allow spinning to the public, you are going to spin to me.”

Such consistency extends to bad news, too. In his 2005 letter he promised shareholders he would “share with you the truth and offer honest assessments of our businesses and our prospects” and that’s something he’s done ever since. Unlike other organisations he doesn’t sugarcoat poor results. At an investor conference at the end of 2009 he said, “I read about JPMorgan's results that they were very good; they were not … And that is because some businesses are doing very well and some businesses are doing very poorly. And I am going to show you what those numbers are, because I think they are important.”

Telling the truth also means acknowledging mistakes. At his Syracuse commencement speech in 2010 he told students, “The first step to dealing with mistakes is to actually acknowledge them.” Two years later JPMorgan suffered trading losses in excess of US$6 billion as a portfolio put together by a trader known as the London Whale unwound. Dimon went on to call it “the stupidest and most embarrassing situation I have ever been a part of”. His letter that year listed two pages worth of lessons he pulled from the episode.

After that, he acknowledged that mistakes would continue to happen. “I think it's silly for anyone in the business world to think you're not going to make mistakes. It is not possible in the real world. That's only possible in a fictional world. I just think the mistakes should be smaller, fewer and far between.”

What he didn’t say was that he had learned his lesson. That’s because lessons aren’t always easy to learn. At the Stanford event, Dimon reflected, “It's like you kind of sometimes learn the same lessons over and over. It’s like being in a boxing ring, they say duck, hold your hands up. Yeah well, that’s harder to do than you think.”

One of the reasons it’s so hard is that no two situations are entirely alike and a balance has to be struck between over-reacting to a pattern of events and under-reacting. Dimon once invoked another analogy to explain: “They say a cat that sits on a hot tin plate will never sit on a hot tin plate again. It also won't sit on a cold tin plate. I don't look at things like there is like one single simple lesson.”

Sweating the details

Dimon has an unnerving knack for detail that many other company executives would regard as beneath them beyond a certain stage in their career. He once told USA Today, “Sometimes, all that matters are the details. Sometimes details will sink you. CEOs should drill down.”

Partly, this principle stems from his natural ability to grasp detail, but there’s also something strategic about it.

First, truth is built on details. As soon as he took the reins at JPMorgan, he built an infrastructure for gathering detail. In his 2005 letter he wrote, “It is hard to act on the truth if you do not know what it is.” One of his first actions was to expand the finance function at the bank.

Second, he sees an attention to detail as one of the antidotes to the challenges that confront large corporations. In his 2008 letter he wrote, “If bureaucracy, hubris, lack of attention to detail – or other ailments of large corporations – overwhelm the benefits of size, then failure will ultimately result.” He is perhaps keenly aware that having helped to create it, Citigroup collapsed under a management team who had little grasp of the details underpinning their organisation. (Richard Bookstaber reckons that Citigroup firing Jamie Dimon ranks as one of the costliest single business decisions in the history of time, alongside the purchase of AOL by Time Warner.)

Finally, although he concurs that details are not integral to the job of a leader, he regards them as integral to the job of a manager and he sees himself as both. He told the David Novak Leadership podcast in 2017: “I’m going to separate leadership and management a little bit … In management it’s follow-up, get it done, it’s analytics, it’s get people round the room, it’s follow-up, it’s get on the road, it’s put in the hours, it’s learn, learn, learn. It doesn’t necessarily make you a great leader … Leadership is a lot more about heart and humility and learning and sharing than it is about how smart you are or follow-up or detailed analytics.”

Bureaucracy as a cause of organisational entropy

Dimon has a distaste for bureaucracy. He told the Stanford audience “The things that destroy companies, folks, are bureaucracy and politics.” In charge of a large complex organisation in a highly regulated industry he clearly doesn’t have the flexibility to lower bureaucracy to Silicon Valley levels. But he sees quashing it as a process itself worth following as the second leg to countering the challenges that come with scale.

In his 2017 letter he wrote, “Bureaucracy is a disease. Bureaucracy drives out good people, slows down decision making, kills innovation and is often the petri dish of bad politics. Large organizations, in fact all organizations, should be thought of as always slowing down and getting more bureaucratic. Therefore, leaders must continually drive for speed and accuracy to eliminate waste and kill bureaucracy. When you get in great shape, you don’t stop exercising.”

If speed and accuracy are the ways to tackle bureaucracy, Jamie Dimon has them both covered. Accuracy is embedded in an attention to detail. Speed is a characteristic he also promotes, both in terms of productivity and in terms of decision-making. He is well known for carrying a paper ‘to-do’ list with him wherever he goes. He told David Novak, “I return every email and every phone call almost every day … if I owe you something I write it in that list.” This is consistent with his view, articulated in his first letter at Bank One, that “problems don’t age well; denying them or hiding them guarantees that they will get worse.”

On decisions, he told an audience in late 2008, “You need people who will argue and fight but at one point, say, we’re going to take the hill. Some debates are chicken or steak. It becomes time to eat.”

Thinking like an investor

In his book The Outsiders, author William Thorndike argues that the best CEOs have an ‘investor’s mindset’. When they consider a business decision like an acquisition or the purchase of capital equipment, “they viewed it as investment and when it had attractive returns they did a lot of it”.

Jamie Dimon certainly has an investor’s mindset. In fact, in his 2014 letter he acknowledges that “our ultimate goal is to think like a long-term investor”.

Perhaps, the biggest overlap from a cognitive perspective is that he thinks probabilistically in an effort to manage the trade-off between upside and downside. In his 2017 letter he wrote, “We strive to try to understand the possibilities and probabilities of potential outcomes so as to be prepared for any outcome. We analyze multiple scenarios … So regardless of what you think about the probabilities, we need to be prepared for the possibilities, including the worst case.”

Because of this he understands the difference between price and value. Warren Buffett gave Jamie Dimon a shoutout in his own shareholder letter for 2011. “The first law of capital allocation – whether the money is slated for acquisitions or share repurchases – is that what is smart at one price is dumb at another. (One CEO who always stresses the price/value factor in repurchase decisions is Jamie Dimon at J.P. Morgan; I recommend that you read his annual letter.)”

Jamie Dimon’s own share purchases certainly cement his position as a great investor. Immediately on accepting the role as CEO of Bank One he bought 2 million shares of stock for some $57 million – they were up 30% in a week. As CEO of JPMorgan he has bought in size (i.e. 500,000 share clips) on three occasions – in January 2009, in July 2012 and in February 2016. On all three occasions the stock was close to relative lows, and rose by an average of 45% over the following year.

(It is telling that he chose not to buy stock at the most recent lows.)

Seeing the big picture

Jamie Dimon sometimes comes in for criticism for straying outside of his lines. His shareholder letters venture into discussions about regulation, policy and international relations. Some see these as his manifesto for the position of Treasury Secretary. This may be so (unlike in the UK, the US does not have a House of Lords so there are few other places for successful former executives to go). But they principally reveal his understanding that JPMorgan does not exist in a vacuum and its interactions with policymakers affect how it deals with customers.

In 2011 Ben Bernanke, then Chairman of the Federal Reserve, was giving a speech on bank regulation and Dimon publicly asked, “has anyone bothered to study the cumulative effect of all these things?” How all the pieces fit together is a core part of the way he thinks. This is also reflected in the way he laid out the causes of the financial crisis in his 2008 letter. Unlike others who promoted their pet theories, Dimon put forward a nuanced account that captured multiple elements.

Allied to this way of thinking is a long-term perspective. Dimon knows that “in the financial services world, it is easy to stretch for growth by reducing underwriting standards or taking on increasingly higher levels of risk” (2006 letter) and so he elevates long-term measures of performance above short-term. At his 2020 Investor Day, he said, “I could care less about the one-year effect… Years themselves are artificial. Accounting is artificial when it comes some of these things. We look at economics, the right thing to do, and then we do it.”

More broadly, he appreciates that a short-term perspective fails to capture the lags that take place in a complex system. Dimon gave an example in his 2017 letter: “There are many examples of presidents getting credit or blame for scenarios that had nothing to do with their governing. We simply learned the wrong lessons. And in the short run, we tend to simplistically look for scapegoats instead of solutions.”

Conclusion

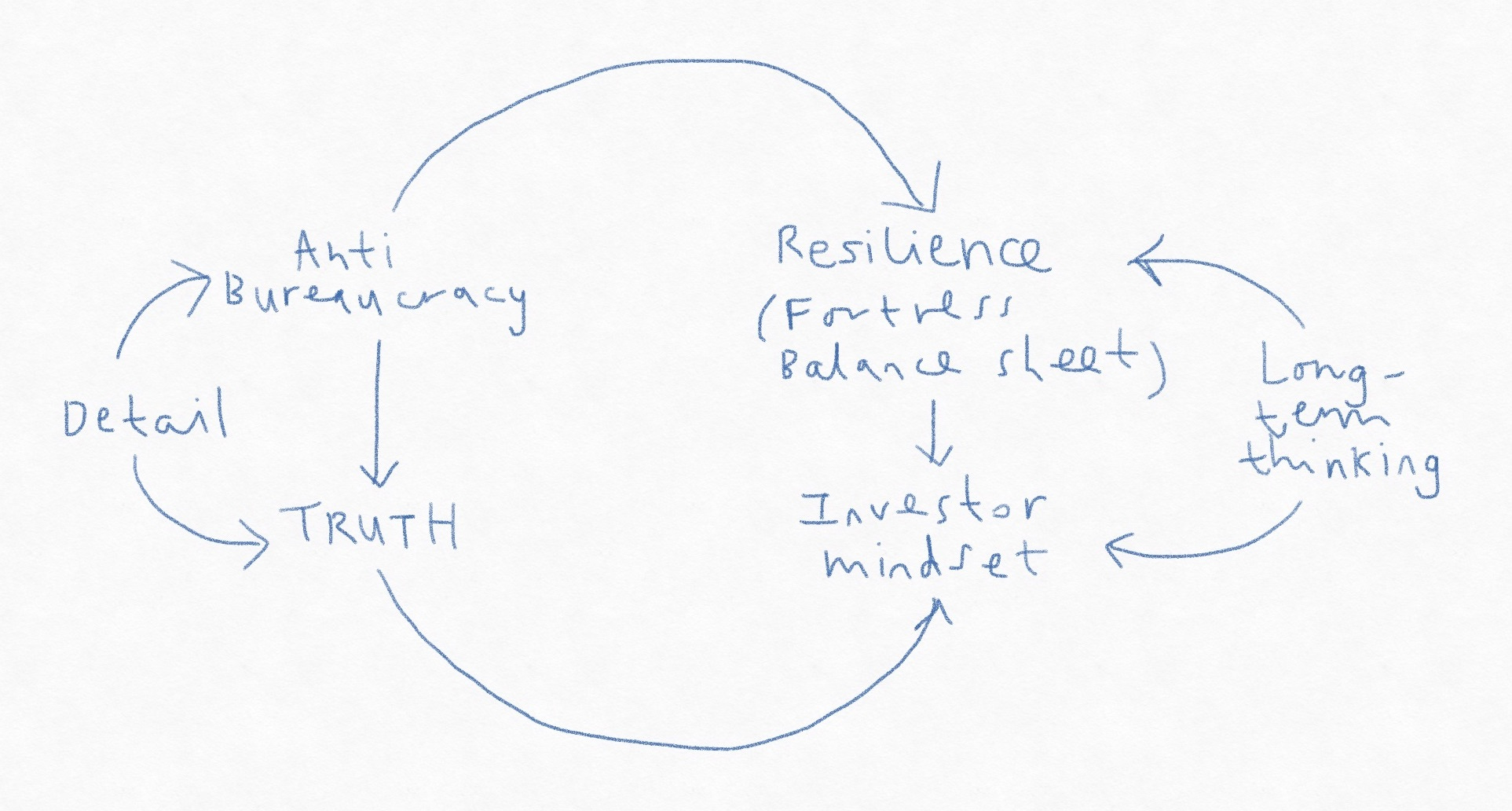

Although I have presented them as distinct ideas, Dimon’s principles all kind of fit together. Fortress balance sheet is consistent with long-term thinking, as is the investor mindset. Detail drives truth and helps stem bureaucracy. Cut it open and Jamie Dimon’s brain might look something like this:

It’s an image that bank CEOs with ambitions to stick around for twenty years may want to take a look at.

Marc Rubinstein is an angel investor in fintech and writes on financial sector themes. He is a former hedge fund manager at Lansdowne Partners, one of the oldest long/short hedge funds in Europe. Prior to that, he was a managing director of Credit Suisse, one of the youngest in his cohort. He started off as an equity research analyst at BZW (investment banking arm of Barclays) specialising in banking sector and moved to Schroeders.

If you enjoy reading Breezy Briefings, please share across social media and tell your friends about it.