Spotify - Reimagining Music

Spotify Technology S.A. (ticker: SPOT, market capitalisation: US$ 23.707B) is a world-leading streaming service that has revolutionised the way people listen to music. Available in 79 countries offering over 50m+ titles, the future of the music industry is online. Spotify offers a unique platform that cannot be easily replicated by its peers, with a subscriber funnel that provides an advertisement laden freemium service that converts listeners to premium accounts at a rate of ~45.76%2 .

Spotify earns revenue through their premium subscribers (~90% of total revenue) and ad revenue from freemium users (~10% of total revenue). The company has experienced revenue increasing at a CAGR of +44.40% from 2013-2019 and has been bolstering its cash balance to maintain its dominant market position with continued investment.

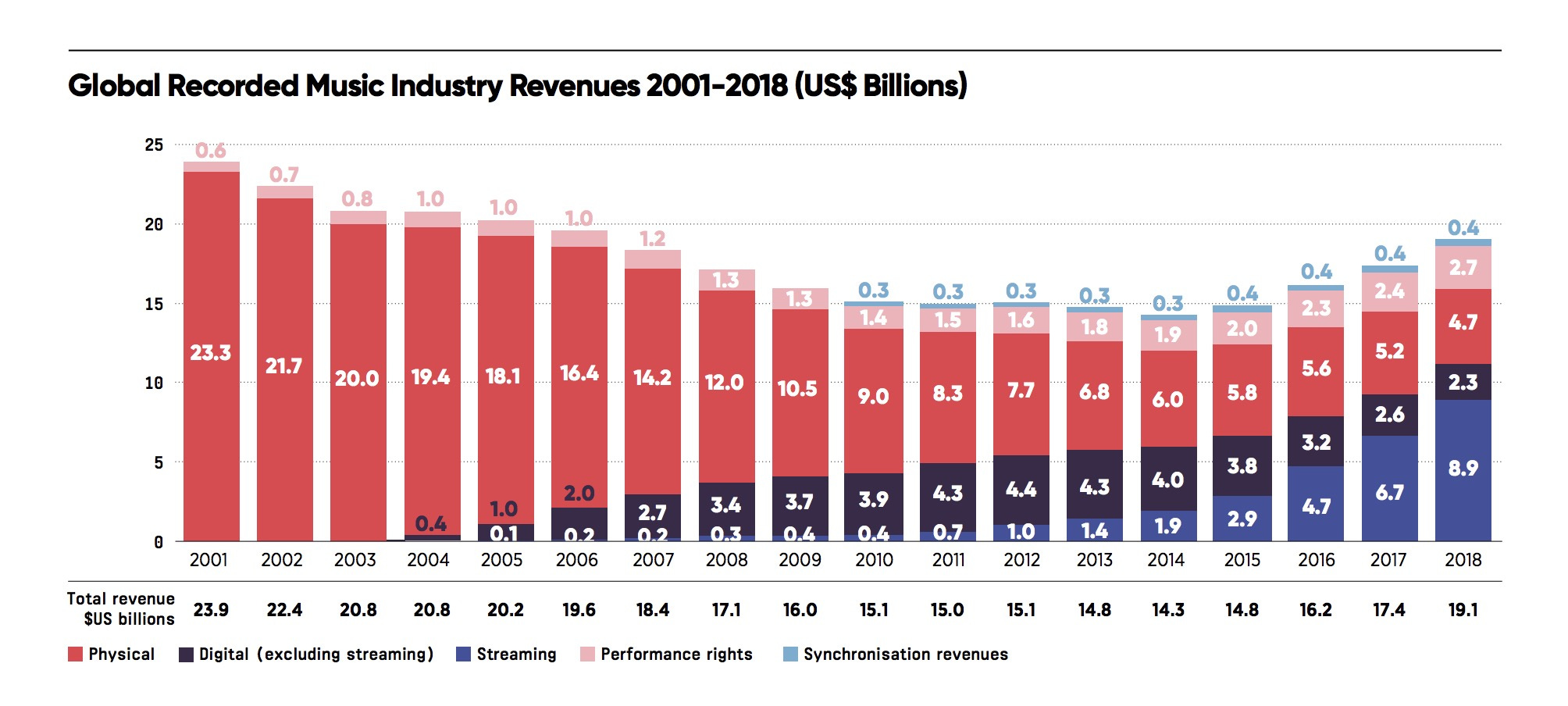

STREAMING HAS REVITALISED THE MUSIC INDUSTRY.

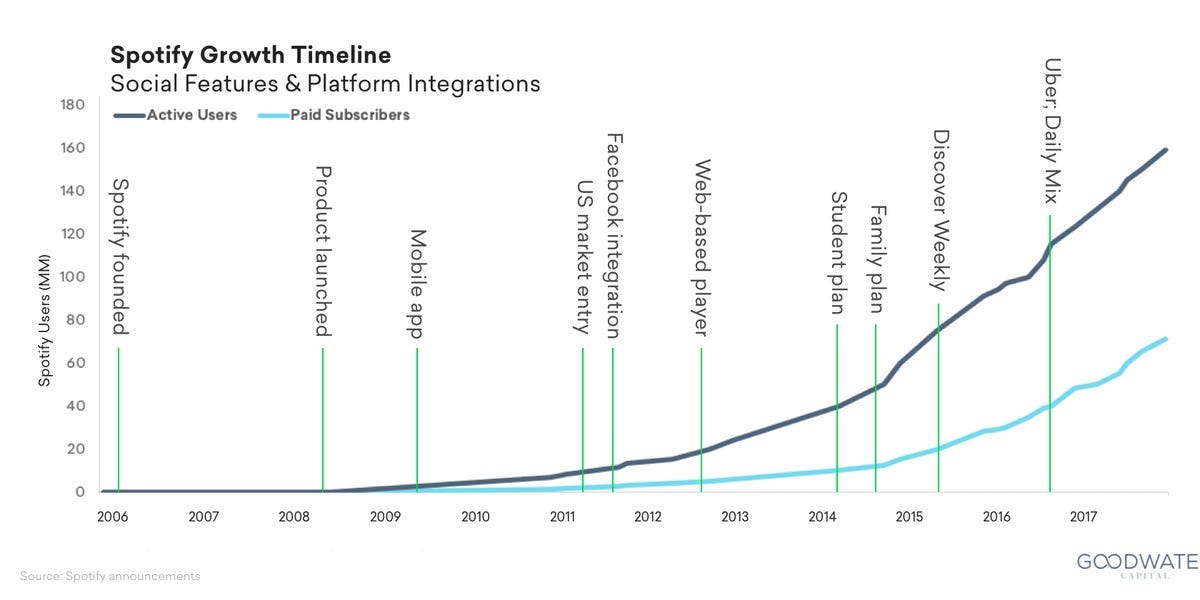

When Spotify launched in Sweden in 2008, the music industry was dying a slow death. In 2001, iPod hit the market providing consumers the ability to select individual songs they wanted to hear, not albums that the record companies seemingly force fed them. From 2001-2008 physical music sales declined at a CAGR of -8% as pirated music became ubiquitous; producers and artists were facing a threat to their livelihood. The introduction of Spotify which today has over 124 million subscribers, 271 million monthly active users (MAU) and over 3 billion playlists, producers and artists were offered a lifeline by once again being able to monetise their music.

Source: IFPI Global Music Report 2019

“The most obvious impact the streaming-driven growth has had on record companies is that it has allowed us to be more aggressive with investment, specifically to invest substantially more in things that directly support artists.” Dennis Kooker - Sony Music Entertainment 2019

OPPORTUNITY IN EMERGING MARKETS.

Growth in mature music markets is slowing, from 2018-2019 the Global Music Market revenue grew by +9.7% driven by Latin America which had the largest year-on-year growth, and Asia which is rapidly becoming a significant consumer. Spotify is already available in 79 countries and is well positioned to benefit from the economic tailwinds appearing globally within these markets. From 2018-2019 Latin America contributed 20% of the company’s MAUs, an increase of 34% from the previous year, while the Rest of the World (excluding Europe and North America which have 40% and 30% MAUs respectively) made up 10%. Spotify earned the majority of its revenue from premium subscribers, which has a direct correlation to the total number of MAUs. From Q4 2018-Q4 2019 MAUs grew by +30.92% from 207 million – 271 million while premium subscribers grew +29.17% from 96 million – 124 million, during the same period revenue grew by +29% from EU€ 5.259B to EU€ 6.764B, highlighting the performance of Spotify’s subscriber funnel incentivising users to become premium users by offering a best-in-class music streaming platform.

CUSTOMER ACQUISITION COMES AT A COST.

For subscriber business models, average revenue per user (ARPU) and lifetime revenue per customer is crucial to maximising revenue while not being too expensive to see user growth continually. Due to increased competition from Apple Music and Amazon, Spotify has been forced to become more aggressive with their offers to sway users away from the competition. Spotify’s strategy includes adding a Premium Family plan for NZ$ 22.50/month which allows up to 6 premium accounts, single-user premium accounts cost NZ$ 14.50/month, and student premium accounts are NZ$ 7.49/month, all premium options offer one month free. To bolster their premium subscribers Spotify has partnered with a number of companies including Spark and AT&T to be included in a bundle. As a result of these package deals, Spotify has seen a reduction in ARPU from EU€ 5.32 in 2017 to EU€ 4.72 in 2019. Benefits of family and student plans often outweigh the short-term loss to ARPU, lifetime revenue per user should increase as family plans have low cancellation rates and students will be reluctant to change providers once they graduate.

BROADEN YOUR MUSIC REPERTOIRE WITH SPOTIFY.

Spotify has been developing its machine learning algorithms to offer a unique music streaming service available. The company prides itself on personalisation and careful curation of playlists that predict what each user wants to listen to, expanding individuals music library with new songs and artists they would never have found otherwise. This feature is not only beneficial to users, but also to artists who give themselves a greater chance of being discovered amongst the crowd of artists vying for clicks. Personalisation represents Spotify’s biggest differential to its competitors. When users log in daily they discover their ‘Daily Mix,’ playlists that group together several artists they frequently listen to with new artists they may like based on genre. Users also receive “Uniquely Yours” offers playlists “On Repeat – Songs you can’t get enough of right now” and “Repeat Rewind – Past songs that you couldn’t get enough of.” Users appreciate this; it’s useful without being invasive and contributes to reductions in electing to use another music streaming service.

It would be nice to see more of an open culture to different music. […]. With Spotify, I think people are discovering a lot of artists they might not discover otherwise. Flume - 2019

UNIQUE TWO-SIDED MARKETPLACE.

For most of Spotify’s corporate life, they have predominantly been a one-sided market place only earning revenue from users. The company has identified potential value in transforming the platform into a two-sided market place which is characterised by economic exchange from two distinct user groups (users and artists) that provide each other with benefits. Spotify is able to monetise data already collected on users which it can offer artists as an advertising platform, whereby the two-sided market place allows artists to make users aware of new releases driving traffic to listen to their music. In Spotify’s February 2020 investor conference call, CFO Paul Vogel noted that users do not consider this type of advertising as a negative, the opt-out rates to receive updates on new releases and artists they may want to listen has been minuscule. By continuing to develop the value created to users and artists, Spotify have a significant moat compared to its competitors by being a platform that services both the sellers and the buyers.

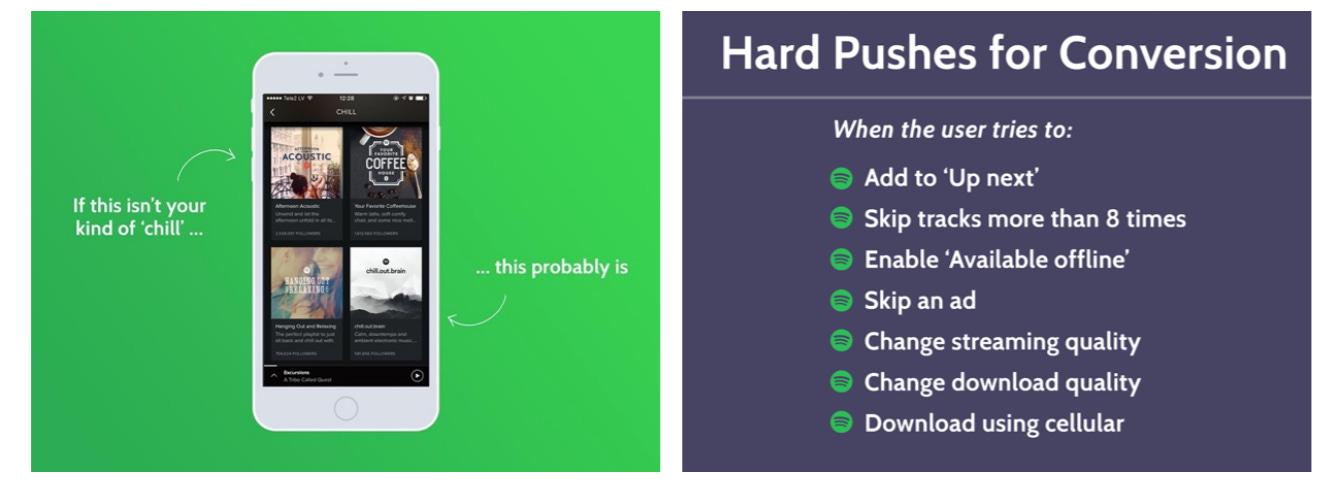

SPOTIFY HAVE A WORLD CLASS SUBSCRIBER FUNNEL.

The primary source of revenue for Spotify’s business model is premium subscribers who currently make up 90% of revenue. The ability to convert free users to premium is a task that Spotify is performing better than its peers. In Q4 2019, premium subscribers grew YoY by +30.92%. Spotify converts users tremendously well achieving a 45.76% conversion rate in Q4 2019, compared to other models that offer a free service, Dropbox has a 4% conversion rate while Google Drive has a 0.5% conversion rate. Spotify have such a well-developed funnel owing to the following:

Reducing sign-up time with Facebook integration making it simple to create an account;

Machine learning playlist curation explicitly tailored to the user with a high degree of accuracy. Free account users are not in control of the music you’re able to listen to. Even if you create playlists, they’re only available on shuffle with a limited number of skips. You can only shuffle and skip so many times before you decide enough is enough; it is time to go premium;

Spotify understands the benefit of music to enhance moods, and situations. Spotify offers descriptive ‘mood’ categories that range from chill to partying and even perfect songs for road trips, finding the perfect soundtrack to make special moments better is a unique selling point offered by Spotify;

When you create playlists, the user is essentially ‘investing’ in Spotify. This investment is more important than a monetary investment, spending time carefully designing playlists for yourself that are not transferrable to any other platform locks users down not wanting to lose their memories;

Going premium allows you to download songs for offline listening, Spotify offers a 30-day free trial to let new users to try this feature. By the end of the thirty days, users see the immense value they’ve created for themselves and do not want to lose all of their work. A lot of free-trial sites are easy to manoeuvre around by merely creating a new email, to do this with Spotify would take hours already invested in finding music all over again;

Offering third-party integration with companies including Nike, Bose, Facebook and even Apple. By enabling usage through a range of devices, Spotify enhances their brand by making their service as available as possible in the competitive marketplace;

A free users journey is carefully designed by Spotify to both subtly and obviously promote the benefit of going premium with calls-to-action (CTA). Several features free users may want to access are discovered to be blocked engraining the necessity of going premium.

PODCASTS OFFER A PATH TO PROFITABILITY.

The market for podcasts is rapidly expanding. Until recently, podcasts grouped into genres ready for listeners to find easily have been scarce. A 2019 PwC report projects that revenues in the podcast industry will top US$ 1 billion in 2021. Spotify has been employing an aggressive strategy to own a significant portion of the market in podcasts with acquisitions of Gimlet Media & Anchor (US$ 340M), Parcast (US$ 55M) and the number one sports entertainment podcast company, Bill Simmons’ The Ringer (US$ 200M). Spotify’s music algorithms and platform are easily transferrable to podcasts, developing a model to enable listeners to discover and listen to podcasts has a lucrative appeal. This model is working, Spotify are currently the podcast leader in over 20 markets globally. Podcast listeners are more engaged, retain and convert to premium at a higher rate, meaning developing this segment of their user base is crucial to long-term profitability goals. By diversifying to podcasts Spotify are becoming the number one audio company for not only music but streaming audio as a whole. Spotify are taking a long-term view, dedicated to capital expenditure to maintain the uniqueness of the service and proactively seizing new opportunities to make it difficult for the competition to keep up. The current business model has limitations. Licensing deals with music companies are expensive and erode their profitability; podcasts represents an opportunity to own the sector by acquiring production companies and developing a vertically integrated model that will help drive profitability.

SPOTIFY - THE FIFTH HORSEMAN.

Scott Galloway explains why Spotify is the Fifth Horseman after Amazon, Apple, Facebook and Google. He cites five key components for becoming a trillion-dollar company:

they must be global;

they must use Machine Learning;

they must have the Benjamin Button Effect in that they get better the more you use them;

they are a likable organisation;

and they must be a career accelerant for young professionals.

All of these are true for Spotify. What truly makes Spotify the Fifth Horseman, is the potential for Spotify to be acquired by Amazon or Apple who want to truly dominate the global music market, which would push Spotify’s value to over US$ 50 billion (EV US$ 22.673B as at 8 April 2020) should it occur.

CONCLUSION.

Spotify has been making global headlines since launching in 2008 when they disrupted the music industry in a way nobody saw coming. Spotify has taken a long-term approach to take advantage of the reappearing economic tailwinds in the audio industry, with the continued development of their service it is not surprising that the company has experienced sustained growth in their user base. Boasting a 45.76% conversion rate, Spotify are positioned to be the number one name in accessing audio online for years to come. We concur with Professor Scott Galloway that Spotify occupies valuable real estate on peoples phones and that accordingly, we believe Spotify is in fact an acquisition target and believe management understand this. Evidenced by them announcing a stock buyback commencing in Q4 2018 reflecting their view the company was/is trading below intrinsic value.

Disclaimer: Not investment advice. For information only. We own this stock

© 2020 Elevation Capital Management Limited

If you enjoy reading Breezy Briefings, please share across social media and tell your friends about it.