We may have passed the point of maximum pain

Abraham George Market Musings

It was an amazing day of the men’s tennis finals at the Australian Open yesterday. For all tennis lovers, you couldn’t have seen a better display of sheer grit, tenacity, experience, battling the odds and competitive psychology. In the end, the last man standing was Raffa going beyond Djokovich and Federer to win 21 grand slams.

Having already won 62% of his grand slams at the French Open, there was every chance Raffa would win again this year taking the tally to 22 Grand Slams. Djokovich may find that hard to beat and Raffa can probably go down in history as the greatest tennis player of all times. But never say never to Djokovich. So much for sports - let’s get to the markets now!

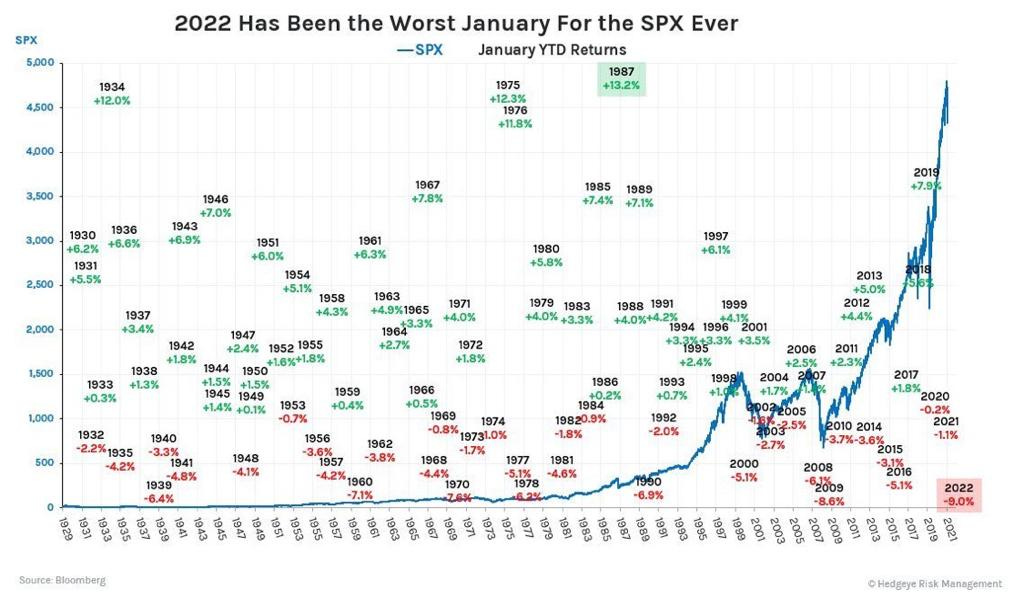

Since mid-November last year, the markets have been more volatile than the previous months and lost for direction. Markets have been very conscious of a possible market top and many participants have been positioning accordingly. The beginning of the year has posted the highs of the year so far and the subsequent fall in January so far is the worst January ever in the history of the stock markets. Take a look at the chart below:

Most of you have heard the old stock market adage, “As goes January, so goes the year.” That may be true and my last report was all about one thing that we are sure of this year is in seeing increased volatility.

I am not much into predictions like many of the well-known veteran fund managers and market commentators. I look at markets from all angles that I understand from my 45 odd years of observations and practical experience to make an informed decision that I think could play out best. At the end of the day, we are not dealing with anything black and white but mostly shades of grey. There is nothing certain here, we are always dealing with probabilities. But experience and longevity in the markets matter when the field of economics is titled as a dismal science.

I am stepping out of my comfort zone to say that the events of the last few months make me conclude that we could see a significant rise in equity prices in the next three months to six months before we see a significant fall. This rise could be something more significant than anything we have seen in the recent past. While one needs to be very aware of the sectors that you should be involved in and why some sectors, in particular, the rise in equities could be across the board.

Before I explain the reasons we will take a look at what we predicted last year and how it played out.

Help us grow 🌱

If you enjoy Breezy Briefings, there are three things you can do to help us grow and reach more people. Which would be lovely!

Share it with someone else. Forward the email. Post on social.

Click/tap the little ❤️ icon at the top or bottom. It actually helps.

For over five years, I have consistently argued that the biggest opportunities and disruptions will come through the digital space and the biggest changes will take place in India as India is rising from a much lower base. I penned the first draft of A Case for Investing in India about five years ago (and it was published in Breezy Briefings 2 years ago).

I also emphasized that many Indian-born companies will emerge on the international scene as service providers, innovators, and solution providers. We are already seeing that with the first Indian-born company, Freshworks, directly being listed on the NASDAQ and many second-tier digital companies like Mindtree, Affle, 3i Infotech, Subex, Route Mobile, Kellton Tech to name a few have already made an international presence.

Tanla Platforms which already have a very strong India presence is now going global. India has made the biggest improvements in the digital space in the last three years and this will continue to grow exponentially. India has been the best performing market last year.

Even before the climate issues could become a major talking point, I gave a bullish call on oil. When Biden was elected President, I labeled going long oil as the ‘no-brainer trade’ (27 Apr 2021) and wrote every weakness in oil is a buying opportunity. So far, I have been right on that. Check my reports on oil dated 30 June 2021, 12 Oct 2021, 27 Nov 2021, and as way back as 17 Feb 2021.

I was very critical of Fed Chairman Jay Powell’s position on transitory inflation and was even more emphatic in announcing that he will change his position down the line and he did. I outlined the risks of Powell being reappointed and how a new Chairman could go along with the present administration. I also concluded that if Powell is reappointed we will see a new style of communique from him which we are already seeing now (see all those reports here, here, here, here, here, and here).

I pointed to the risks of a market correction but hesitated to commit to the depth of the correction. Now, I like to think that we may have passed that stage of maximum pain and hopefully sunnier days might be in store for us.

If you received value from this post, and you’d like to send some back, or if you’d like to signal to me to continue spending time on these types of explorations, feel free to buy me coffees (thank you!):

So, there we go. Thanks for reading Breezy Briefings. If you enjoyed this, I'd really appreciate it if you could take a second and tell a friend. Honestly. It makes such a big difference.

Forward this email. Recommend the newsletter. Share on Twitter, WhatsApp, Telegram, LinkedIn, Slack, wherever!

Join Breezy Briefings’ Official Telegram Channel: https://t.me/BreezyBriefings

Abraham George is a seasoned investment manager with more than 40 years of experience in trading & investment and multi-billion dollar portfolio management spanning diverse environments like banks (HSBC, ADCB), sovereign wealth fund (ADIA), a royal family office and a hedge fund. Currently, he is a co-founder of a new hedge fund where foreign citizens can invest in Indian growth stocks like Tanla operating in hyper-growth markets like CPaaS.